Introduction

Buying a car is one of the most significant financial decisions for individuals and families. While cars provide convenience, mobility, and independence, the cost of purchasing a vehicle can be high. Many people may not have enough savings to pay the full price of a car upfront. This is where car loans play an important role in modern personal finance.

A car loan is a type of secured loan provided by banks or financial institutions to help individuals purchase a vehicle and repay the amount over time through monthly installments called Equated Monthly Installments (EMIs). Instead of paying the entire amount at once, borrowers can spread the cost over several years while using the car immediately.

This guide explains everything you need to know about car loans, including types of car loans, features, eligibility requirements, documents required, EMI calculations, factors affecting approval, and how to apply for a car loan.

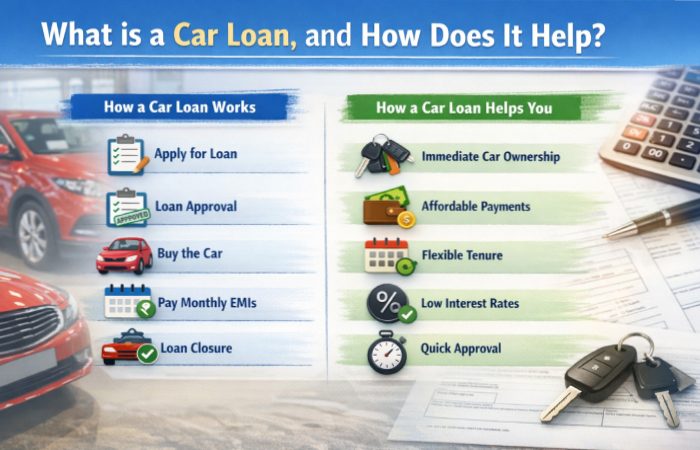

What is a Car Loan, and How Does It Help?

A car loan is a financial product that allows individuals to borrow money from a bank or financial institution to purchase a vehicle. The borrower repays the loan amount along with interest over a predetermined period.

In most cases, the car itself acts as collateral (security) for the loan until the full repayment is completed.

How a Car Loan Works

| Step | Description |

| Loan Application | The borrower applies for a car loan with a bank or lender |

| Eligibility Check | The lender checks credit score, income, and employment stability |

| Loan Approval | Once approved, the bank sanctions the loan amount |

| Car Purchase | The bank pays the dealer directly |

| EMI Repayment | Borrower repays monthly EMIs including principal and interest |

| Loan Closure | After repayment, full ownership is transferred to the borrower |

How a Car Loan Helps Buyers

| Benefit | Explanation |

| Immediate Car Ownership | Buy a car without paying the full cost upfront |

| Affordable Monthly Payments | Spread the cost over several months or years |

| Flexible Loan Tenure | Most loans range from 1 to 7 years |

| Competitive Interest Rates | Lower interest rates than personal loans |

| Quick Processing | Many banks approve loans within hours |

Car loans are especially helpful for individuals who want to maintain financial liquidity while still purchasing a vehicle.

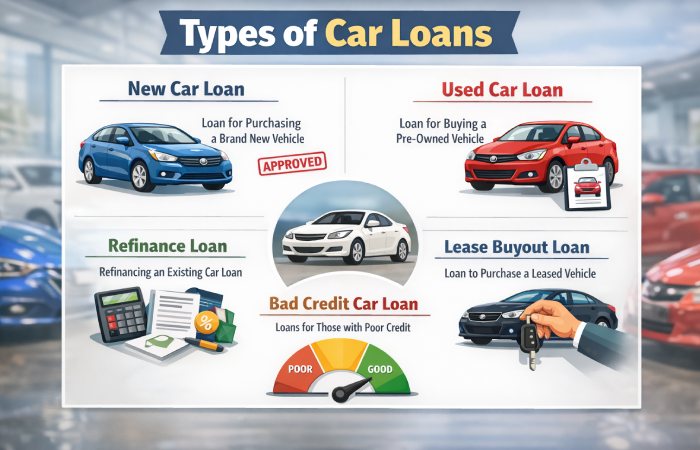

Types of Car Loans

Financial institutions offer several types of car loans depending on the borrower’s requirements and the vehicle type.

Common Types of Car Loans

| Loan Type | Description |

| New Car Loan | Financing for brand-new vehicles |

| Used Car Loan | Loans designed for second-hand vehicles |

| Loan Against Car | Borrow money using an existing car as collateral |

| Dealer Financing | Loan arranged directly through a car dealership |

| Lease Buyout Loan | Used to purchase a leased vehicle at the end of the lease |

Comparison of Car Loan Types

| Loan Type | Interest Rate | Loan Tenure | Loan Amount |

| New Car Loan | Lower | Up to 7 years | Up to 90% of car value |

| Used Car Loan | Higher | Up to 5 years | Up to 80% of value |

| Loan Against Car | Moderate | Up to 5 years | Depends on vehicle value |

| Dealer Financing | Varies | Flexible | Based on dealer partnership |

Used car loans generally have higher interest rates because lenders consider them slightly riskier than loans for new vehicles.

Features and Benefits of Car Loan

Car loans come with several features that make them attractive to borrowers who want flexible financing options.

Key Features of Car Loans

| Feature | Description |

| High Financing | Up to 90% of the car’s on-road price |

| Long Tenure | Loan repayment up to 7 years |

| Flexible EMI Options | Monthly installments based on tenure |

| Quick Disbursement | Loans may be approved within 24–48 hours |

| Online Application | Easy digital application process |

Some banks also allow financing for insurance, accessories, registration charges, and maintenance packages as part of the car loan.

Major Benefits of Car Loans

| Benefit | Explanation |

| Budget-Friendly Purchase | No need for full payment upfront |

| Improves Credit Score | Timely EMI payments build credit history |

| Flexible Loan Amount | Borrow based on income and eligibility |

| Tax Advantages | Business owners may claim deductions |

| Easy Approval | Simple documentation process |

These benefits make car loans one of the most popular forms of vehicle financing globally.

Factors Affecting Car Loan

Several factors influence whether a bank approves your loan and what interest rate you receive.

Major Factors Affecting Car Loans

| Factor | Impact |

| Credit Score | Higher score means lower interest rate |

| Income Level | Determines repayment capacity |

| Employment Stability | Stable jobs improve approval chances |

| Loan Tenure | Longer tenure lowers EMI but increases total interest |

| Down Payment | Higher down payment reduces loan amount |

| Type of Vehicle | New cars often receive better loan terms |

For example, borrowers with credit scores above 750 often qualify for lower interest rates because lenders consider them low-risk borrowers.

Additional Factors Considered by Lenders

| Factor | Description |

| Relationship with Bank | Existing customers may get better rates |

| Age of Borrower | Most lenders prefer borrowers under 65 |

| Debt-to-Income Ratio | Lower debt improves loan eligibility |

| Location | Urban borrowers may get faster approval |

Eligibility Criteria

Eligibility criteria vary slightly between lenders, but most banks follow similar standards.

General Eligibility Requirements

| Criteria | Requirement |

| Age | 21–65 years |

| Employment | Salaried or self-employed |

| Minimum Income | Depends on bank policy |

| Credit Score | Ideally 700 or higher |

| Work Experience | Minimum 1–2 years |

| Residence Stability | Permanent address proof |

Eligibility Comparison

| Applicant Type | Income Proof | Work Experience |

| Salaried | Salary slips and bank statements | 1–2 years |

| Self-Employed | Income tax returns | 2–3 years business history |

Meeting these requirements increases the chances of faster loan approval.

Documents Required

To process a car loan, lenders require documents to verify identity, address, and income.

Identity Proof

Accepted Documents

- Aadhaar Card

- PAN Card

- Passport

- Voter ID

Address Proof

Accepted Documents

- Utility bills

- Aadhaar card

- Passport

- Rental agreement

Income Proof

| Salaried Individuals | Self-Employed Individuals |

| Salary slips (3 months) | Income tax returns |

| Form 16 | Business registration |

| Bank statements | Profit & loss statement |

These documents help lenders verify the borrower’s ability to repay the loan.

Car Loan EMI Calculator

A Car Loan EMI Calculator helps borrowers estimate monthly payments before applying for a loan.

The EMI is calculated using the following formula:

EMI = [P × R × (1+R)^N] / [(1+R)^N − 1]

Where:

| Variable | Meaning |

| P | Loan amount |

| R | Monthly interest rate |

| N | Loan tenure in months |

This formula is widely used by banks and online calculators to estimate EMI amounts.

Example EMI Table (Approx.)

| Loan Amount | 3 Years | 5 Years | 7 Years |

| ₹5,00,000 | ₹16,016 | ₹10,501 | ₹8,192 |

| ₹8,00,000 | ₹25,626 | ₹16,802 | ₹13,107 |

| ₹10,00,000 | ₹32,033 | ₹21,002 | ₹16,384 |

| ₹15,00,000 | ₹48,049 | ₹31,503 | ₹24,575 |

These EMI estimates assume an average interest rate of around 9.5% per year.

What You Should Know Before Taking a Car Loan

Before applying for a car loan, it is important to evaluate the financial impact of the loan.

Important Tips for Borrowers

| Tip | Explanation |

| Compare Lenders | Check multiple banks before choosing |

| Check Processing Fees | Some lenders charge 0.5%–2% |

| Understand Total Cost | Interest adds significant cost |

| Maintain Good Credit Score | Helps secure lower rates |

| Avoid Long Tenure | Long tenure increases total interest |

Loan Planning Checklist

| Question | Why It Matters |

| Can I afford the EMI? | Prevent financial stress |

| Do I have enough down payment? | Reduces loan burden |

| What is the total interest payable? | Understand total cost |

| Are there prepayment penalties? | Important if you plan early closure |

Even a 1% difference in interest rate can significantly increase total loan cost, especially for long-term loans.

Top Car Loan Interest Rates with Bank Name

Below is a comparison of car loan interest rates offered by major banks in India.

New Car Loan Interest Rates

| Bank | Interest Rate | Maximum Tenure |

| State Bank of India | 9.00% – 9.70% | 7 years |

| HDFC Bank | 9.20% – 11.75% | 7 years |

| ICICI Bank | 9.50% – 12.25% | 7 years |

| Axis Bank | 9.30% – 12.00% | 7 years |

| Kotak Mahindra Bank | 9.25% – 11.50% | 7 years |

Used Car Loan Interest Rates

| Bank | Interest Rate | Max Tenure |

| HDFC Bank | 12% – 16% | 5 years |

| ICICI Bank | 12.5% – 16.5% | 5 years |

| Axis Bank | 12.25% – 16.25% | 5 years |

These rates may vary depending on credit score, income level, and loan amount.

How to Apply for a Car Loan?

Applying for a car loan is straightforward and can be completed either online or at a bank branch.

Step-by-Step Application Process

| Step | Description |

| Step 1 | Compare car loan offers from multiple banks |

| Step 2 | Check eligibility and interest rate |

| Step 3 | Submit loan application form |

| Step 4 | Upload or submit required documents |

| Step 5 | Bank verifies credit and income |

| Step 6 | Loan approval and disbursement |

Online vs Offline Application

| Method | Advantages |

| Online Application | Faster approval and paperless process |

| Bank Branch | Personal assistance and consultation |

| Dealer Financing | Convenient during vehicle purchase |

Many banks now provide instant pre-approval through online applications, making the process faster and more convenient.

Conclusion

A car loan is a convenient financial tool that allows individuals to purchase vehicles without paying the full price upfront. With flexible repayment options, competitive interest rates, and fast approval processes, car loans have become a popular financing option for millions of buyers.

However, borrowers should carefully evaluate factors such as interest rates, loan tenure, EMI affordability, and total repayment cost before applying. Comparing different lenders and maintaining a good credit score can help secure better loan terms.

By understanding the loan structure and planning finances wisely, borrowers can enjoy the benefits of car ownership while maintaining long-term financial stability.

FAQ

What credit score is required for a car loan?

Most lenders prefer a credit score of 700 or above to offer competitive interest rates.

Can I get a car loan with zero down payment?

Yes, some banks offer 100% financing, but interest rates may be slightly higher.

What is the maximum tenure for a car loan?

Most banks provide a maximum repayment period of 7 years (84 months).

Can I prepay a car loan early?

Yes, many lenders allow prepayment or foreclosure, although some may charge a small fee.

Is a car loan better than a personal loan?

Yes, car loans usually have lower interest rates because they are secured loans backed by the vehicle.